What is Auto Insurance?

Auto insurance policy is mandatory for vehicle owners as per Indian Motor Vehicles Act 1988. This Plan is designed to give coverage for losses which insured might incur in case his gets stolen or damaged. The amount of Auto insurance premium is decided based on the Insured Declared Value of a car. The premium will increase, if you raise the IDV limit and vice versa.

Why do I need to insure my vehicle?

Auto insurance is mandatory for all vehicles that ply on roads-like car, trucks, etc. The prime objective of this type of insurance is to provide complete protection & coverage on physical damage or loss from man-made & natural disasters. According to Indian Motor Act 1988, an auto insurance policy is mandatory for every automobile owner in the country. Hence, purchasing an auto insurance is not just a necessity, it is mandatory by law.

Key Features of Auto Insurance

| Accident | Fire | Lightening | Explosion |

| Self-Ignition | Transit by Rail, Road, Air & Elevator | Theft | Terrorism |

| Earthquake | Riot & Strikes and / or Malicious Acts | Flood, Cyclone | Inundation |

Types of Auto Insurance

1)Car Insurance

This insurance gives coverage against accidental damage or losses to the holder’s vehicle or third party. The amount of premium depends upon the make of the car, manufacturing year, value & state of registration.

2)Two Wheeler Insurance

This type of insurance is for scooters, bikes & features are similar to that of four-wheeler insurance.

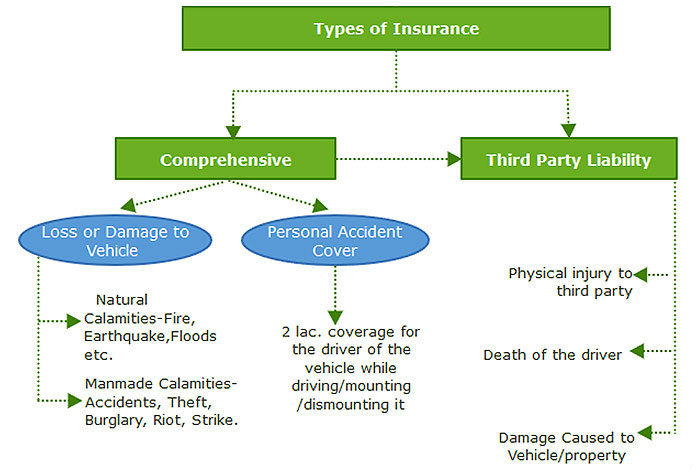

3) Comprehensive Coverage

This type of coverage offers complete package policy wherein any damages to the vehicle will be covered up to the Insured Declared Value. Any third party property damage or third party injury/death can be covered. Policyholders feel less stressful as it gives end-to-end coverage.

4) Third Party Liability Coverage

Under the Motor Vehicles Act, third party liability coverage is legally mandatory. This type of auto insurance offers coverage against all legal liabilities to a third party caused when insured vehicle owner is at-fault. It insures injury/damage caused by policyholder to third person/property

5) Collision Coverage

It financially protects the policyholder against damage of insured’s own car. Collision coverage pays the policyholder for damage caused because collision which generally occurs due to an accident.

Add-On Riders

Add-on riders doesn't take the depreciation value of the parts & allows you to receive the entire claim amount. It is generally available for cars under three years & allows eligibility to claim full amount for replacing/changing any damaged parts of your vehicle.

Exclusions from Auto Insurance

Important points to remember in the event of an accident

These documents must always be in your vehicle:-

To Initiate The Claim Process